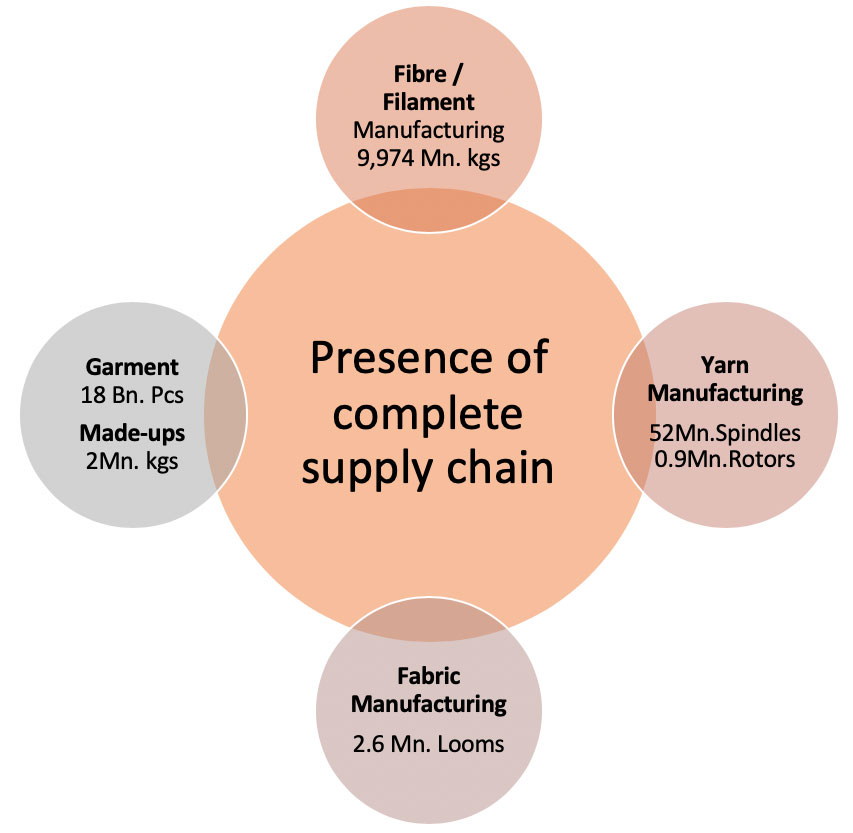

India is one of the few textile manufacturing countries in the world where all levels of textile value chain i.e. from fibre/ filament to garment/made-ups manufacturing are present.

Figure: Indian textile manufacturing value chain

In contrast, countries like Bangladesh, Vietnam, Sri Lanka, Myanmar, Ethiopia and Cambodia have fragmented value chains; mostly focused on end-product and dependency on the other countries for fabric and yarn.

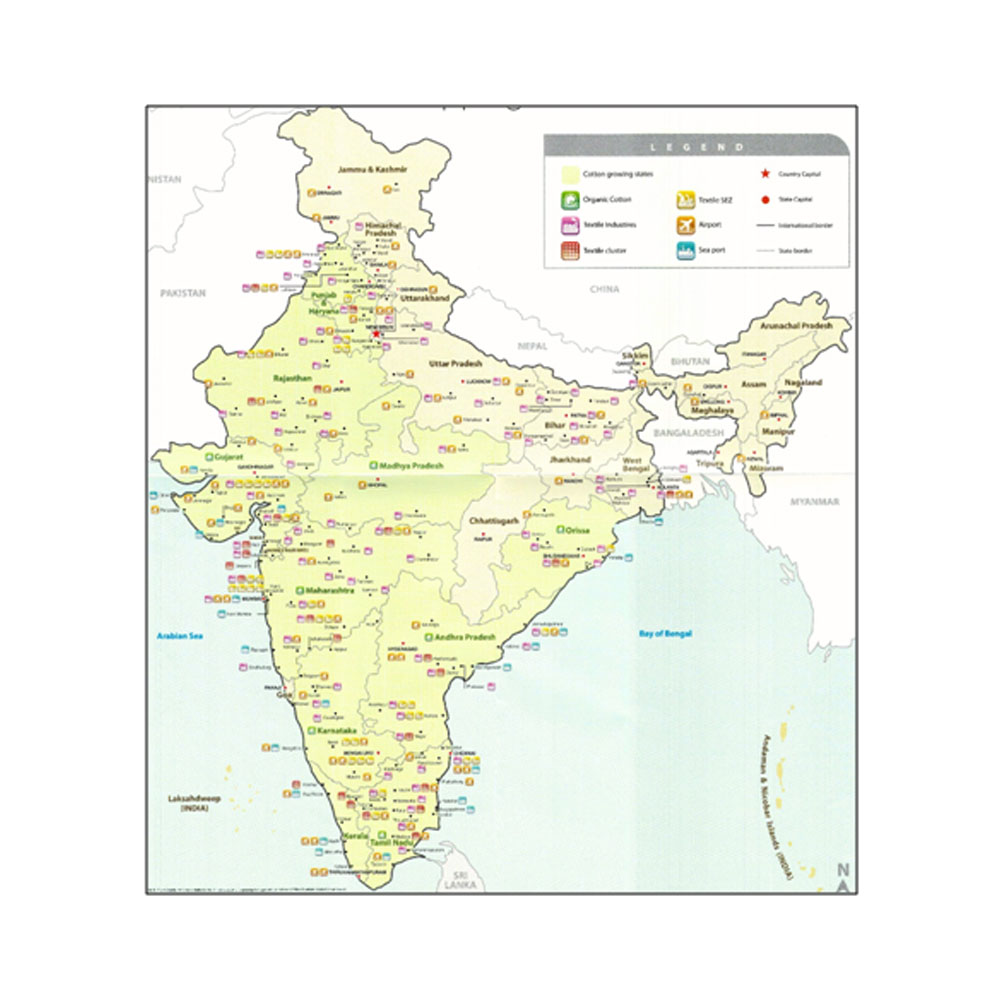

India has a long tradition of textile and apparel manufacturing with infrastructure spread across the country in various clusters. Few important industry clusters are depicted below:

Figure: India’s Textile & Apparel Clusters

In addition to the traditional, natural manufacturing clusters, new virtual clusters are being developed with support from Indian central and state governments in form of textile and apparel parks. Till date, central government has sponsored 66 such parks across states which are at various stages of implementation.

Special Economic Zones (SEZ) is another form of support that aids the textile and apparel exporters to be globally competitive. Indian central and state governments also support in the establishment of Centres of Excellence (CoEs), R&D facilities, etc. which are key infrastructure tools for the growth of textile industry.

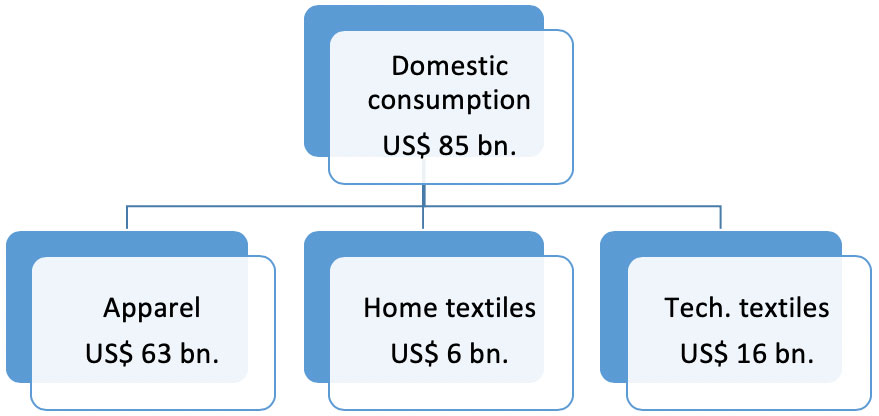

The Indian domestic consumption of textile and apparel is valued at US$ 85 bn. in 2016. Within this, apparel retail contributes US$ 63 bn., technical textiles contribute US$ 16 bn. and home textiles contribute US$ 6 bn.

Figure: Indian Domestic Textile and Apparel Consumption (2016)

Source: Wazir Analysis

In last decade, Indian domestic market has performed better than the largest consumption regions like US, EU and Japan, where depressed economic conditions led to lower demand growth. The domestic apparel consumption of India has grown at a robust CAGR of 11% since 2005. Due to presence of strong fundamentals, the domestic apparel market size of India is expected to reach a level US$ 220 bn. by 2025.

Studies show that countries after achieving a per capita GDP of more than US$ 2,500 experience a spur of economic growth led by consumer spending. The Indian economy is expected to reach this target by 2020. This will help in exponential growth of textile and apparel consumption with the country. Beyond the increasing income of Indian consumers that is making them buy more, and better; the market growth will be led by following important drivers: