Annual Report Indian Textile & Apparel Industry 2023

Contents

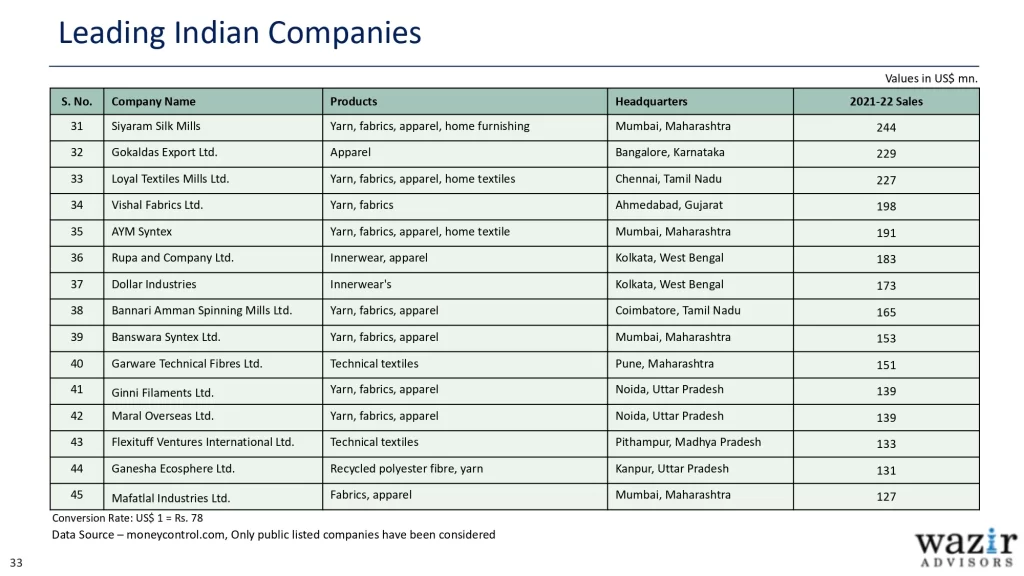

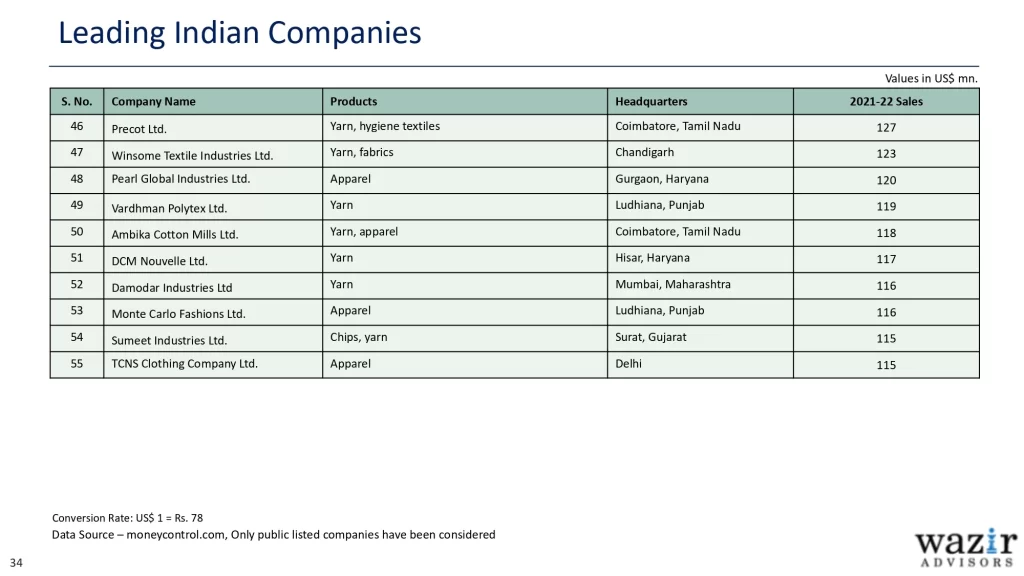

• Global Sector Overview – 03 • Indian Sector Overview – 10 • Indian Industry Structure and Supply Scenario – 17 • Leading Indian Companies – 30

Disclaimer

This document is a copyright of Wazir Advisors Private Limited, India. No part of this publication may be reproduced, stored in, or introduced into a retrieval system, or transmitted in any form or by any means (electronic, mechanical, photocopying, recording or otherwise), without the prior written permission of Wazir Advisors. We have made every effort to ensure the accuracy of information presented in this document. However, neither Wazir Advisors nor any of its office bearers or employees can be held responsible for any financial consequences arising out of the use of information provided herein. In case of any discrepancy, error, etc., same may please be brought to the notice of Wazir Advisors for appropriate corrections.

Key Happenings

Soft Global Demand due to High Inflation and Economy Slowdown • High inflationary conditions and recessionary trends in key markets of US and EU kept the textile and apparel demand subdued in 2022, especially the later half. Volume growth in most of the markets remained in negative to nil zone, with market size increase happening due to higher product costs.

Raw Material Price Volatility • 2022 was marked with unprecedented raw material price volatility. The daily Cotlook index reported highest value of 173 in May (highest value in more than a decade), which then almost halved down to 89 in November. Manmade fibre price variation during the year also remained high, although not as sharp as cotton. This volatility caused uncertainties in the downstream value chain, which was exacerbated by buyers’ ‘wait and watch’ approach in wake of low consumer confidence.

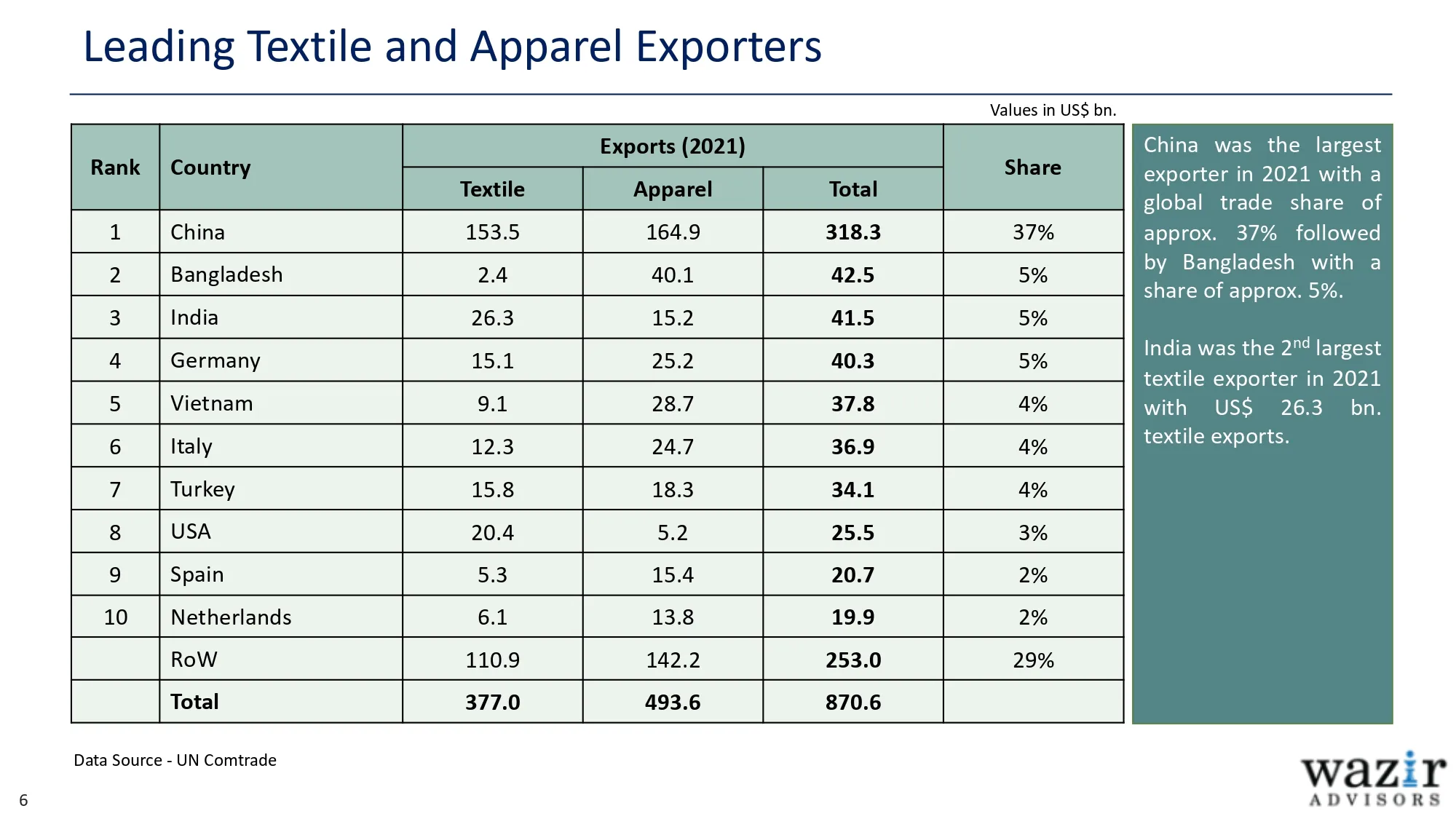

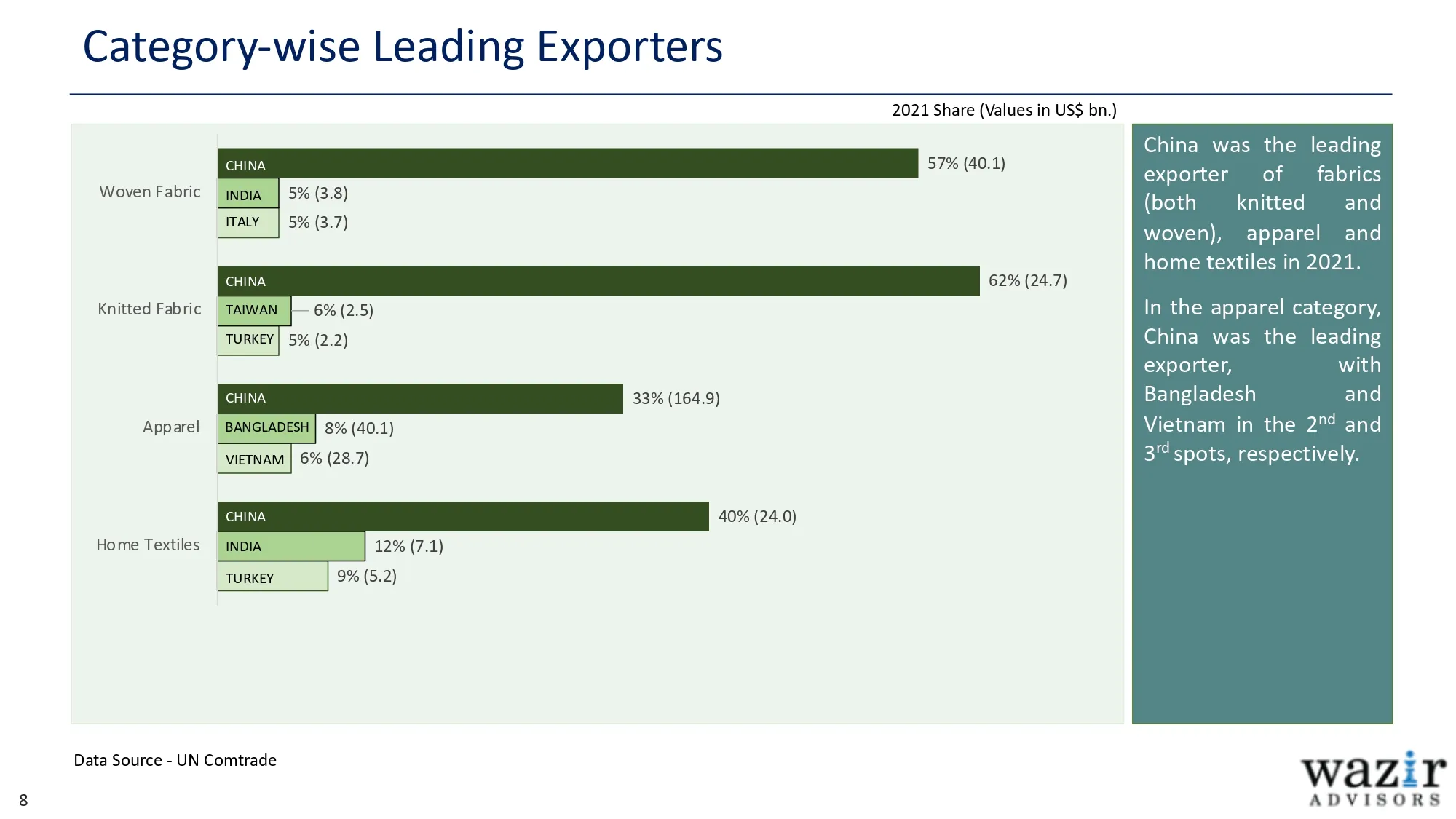

China’s Loss Became Bangladesh and Vietnam’s Gain • China continued to lose its share in the global textile and apparel exports because of rising cost of manufacturing and geo political shifts. Bangladesh and Vietnam emerged the highest gainers of China’s lost share, successfully catering to global fashion buyers looking for supply base diversification.

EU’s Sustainability Legislation Announcement • In March 2022, the European Commission published “EU Strategy for Sustainable and Circular Textiles” with a vision to produce, distribute and consume textile and apparel products sustainably by 2030. The alignment with this legislation will be important for manufacturers and brands alike, to keep up and stay competitive.

Key Happenings

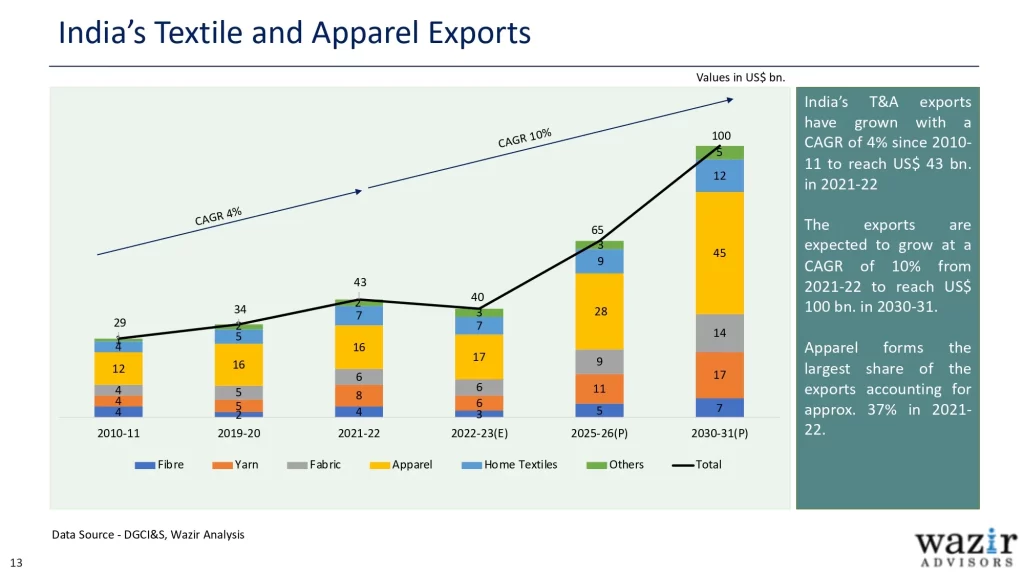

Exports Went for a Rollercoaster Ride • Indian textile and apparel exports started the year on a strong note. In the first half of 2022, they crossed US$ 20 bn. (12% higher over same period in 2021) hinting at all time highest exports, but in the later half they declined dramatically. T&A exports in 2022 are expected to be 8-10% lower than the last year.

FTA Signing and Discussions • India concluded two FTAs in 2022; with UAE and Australia. The most anticipated one, with the UK, however, could not be signed and is on cards for 2023. Also, India and Canada resumed FTA negotiations after a gap of almost five years and discussing an interim trade deal first.

New State Textile Policies • In 2022, Bihar joined the list of Indian states that have dedicated textile sector policies. The states of UP and Odisha released their new textile policies, after expiry of the previous ones.

Central Government Initiatives • 64 projects in manmade value chain (fabrics, garments an technical textiles) were approved under Production Linked Incentive (PLI) Scheme with a cumulative investment of approx. US$ 2.5 bn. In October, Ministry of Textiles released a draft of the Production Linked Incentive 2.0 scheme. • Under National Textile Technology Mission (NTTM), 63 new projects were approved in 2022 with a total project cost of approx. US$ 20 mn.