The presence of a strong textile manufacturing base in India puts India among the leading fabric producing countries in the world and sets up a perfect base for the industry to grow further. Also, various other factors have further contributed in supporting and increasing the demand of woven fabric in India, which include:

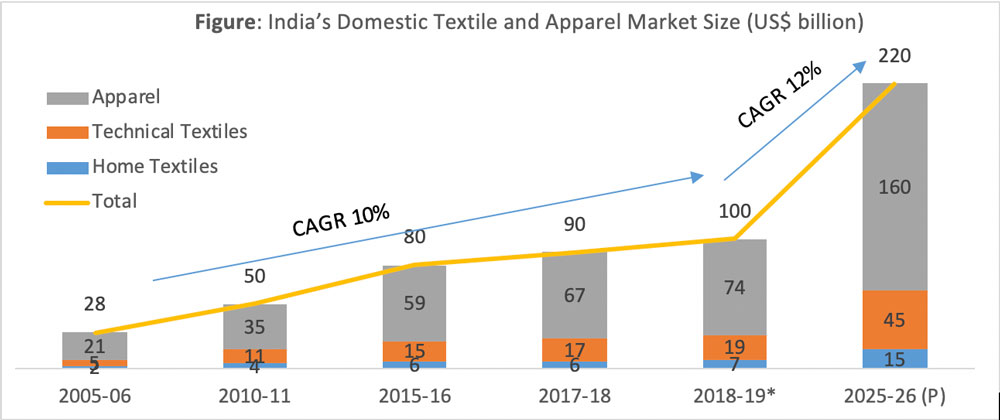

Apparel: India’s domestic textile and apparel market is estimated at US$ 100 billion in 2018-19 and has grown at a healthy CAGR of 10% since 2005-06. The market is further expected to reach US$ 220 billion by the year 2025-26, growing at an even stronger CAGR of 12%.

Data Source: Ministry of Textiles & Wazir Analysis * Estimated

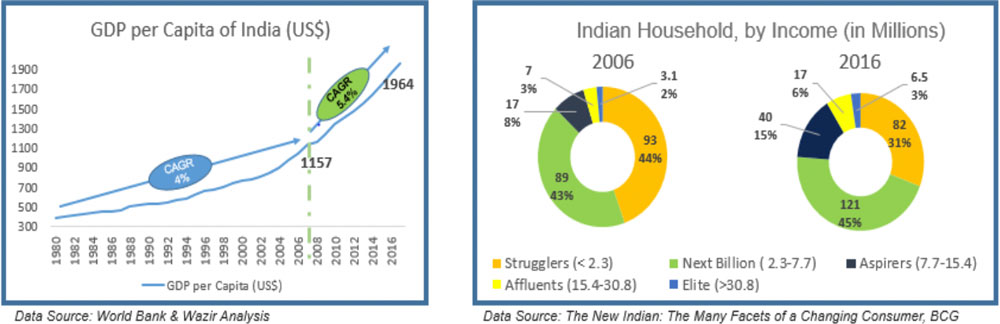

Growth in Income: India’s Per Capita Income has seen a significant growth in the last decade. India’s per capita GDP has grown at rate of CAGR 4.5% since 1980. However, the growth since 2008 has been fairly rapid at 5.4% CAGR. Also since 2006, the number of households in India which earn $2,300- $7,700 has increased significantly from 89 million households to 121 million households in 2016. For the apparel industry this translates to increase in the spending capacity of the consumers along with an increase in the customer base.

Fast Fashion: The modern fashion trends like fast fashion have led to an increased demand of economical apparel with high fashion content, which in turn has led to an increase in the frequency of apparel purchase. In the coming years, similar trends are expected to continue governing the apparel industry.

Hospitality Business: Hospitality industry is a major consumer of woven products, with the use of products ranging from bed sheets and coverings to towels and curtains. India in the last two decades has seen a huge growth in the number of hospitals and hotels, which in turn has led to an increase in demand of woven textiles.

Diversification: The consumption of apparel in India has not just grown in basic categories, but has led to a diversification of products into newer categories. Product categories like loungewear, evening wear, sportswear and activewear. An average Indian wears at least 2-3 different pairs of apparel throughout a day, which is another major growth driver for the industry.